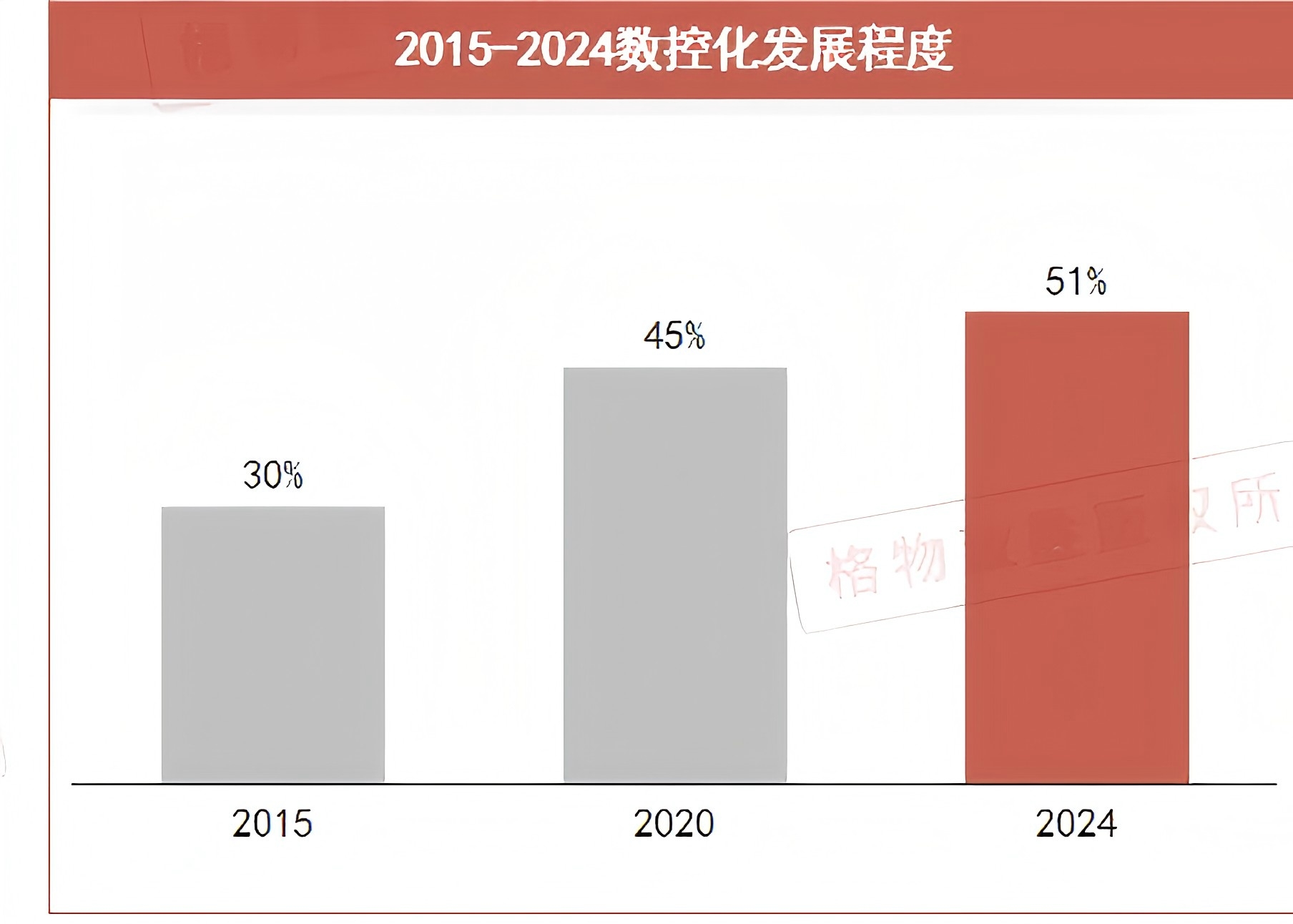

Machine tools, as the "mother machines" of industry, are the foundation and core equipment of manufacturing. Their development level is directly related to a country's industrial strength. In recent years, as China's manufacturing industry has transformed towards high-quality development, the machine tool industry has also undergone profound changes. This article will comprehensively analyze the current market situation, policy environment, competitive landscape, and future trends of China's machine tool industry in 2025, revealing the industrial logic behind the increase in the numerical control rate to 51%, as well as how domestic machine tool enterprises can break through in the waves of high-end and intelligent development. I. Analysis of the Current Situation and Market Size of China's Machine Tool IndustryAfter years of development, China's machine tool industry has established a complete industrial system and has become the world's largest producer and consumer market for machine tools. In 2024, despite the downward pressure on the global economy, the overall market size of China's machine tool industry still reached 1,040.7 billion yuan, demonstrating strong industrial resilience. This scale is closely related to the huge volume of China's manufacturing industry. As the "workhorse" of the equipment manufacturing industry, the demand for machine tools is highly correlated with the prosperity of the manufacturing industry. From a segmented market perspective, the metal cutting machine tool, metal forming machine tool, machine tool functional components and accessories, and other sub-sectors achieved growth, while the abrasive and grinding tools sub-sector continued the downward trend of the previous year, with a year-on-year decline of 15%, reflecting the differentiated development trends in different sub-sectors. The digital transformation has become the most prominent feature of the industry. Data shows that the degree of digitalization in China's machine tool industry has risen from 30% in 2015 to 51% in 2024. This leap forward is driven by both national policy guidance and enterprise technological innovation. The "Made in China 2025" plan explicitly sets a target of achieving a 64% digitalization rate for key processes by 2025, while the State Council has an even more ambitious goal of exceeding a 75% digitalization rate for key processes in large-scale industrial enterprises by 2027. These policy directions have created a vast development space for the digital machine tool industry. From a technical perspective, digital machine tools have significant advantages over traditional ones, such as high precision, high efficiency, and good flexibility, which can meet the demands of modern manufacturing for complex parts processing. This is the intrinsic logic behind the continuous increase in their market penetration rate.

From the perspective of import and export data, China's machine tool industry exhibited a trend of "declining imports and growing exports" in 2024, with the trade surplus further expanding. The main reasons for the decline in imports include multiple factors such as insufficient domestic market demand, the strengthened import substitution effect brought about by technological progress, and restrictions imposed by Western countries on the export of high-end machine tools. Notably, five-axis machining centers produced by domestic enterprises represented by Haitian Precision Machinery and Kede Numerical Control have entered the aerospace component industry chain in batches, marking a substantial breakthrough of domestic high-end numerically controlled machine tools in key fields. In terms of exports, products such as metal-cutting machine tools, metal-forming machine tools, and woodworking machine tools all achieved growth. Among them, the exports of metal-forming machine tools and woodworking machine tools even showed double-digit growth, reflecting the gradual improvement of the competitiveness of domestic machine tools in the international market.

In terms of regional distribution, China's machine tool industry presents obvious clustering characteristics. East China, as the most concentrated region for China's machine tool industry, has a complete industrial chain support system and a rich reserve of technical talents. Provinces and cities represented by Shanghai, Jiangsu, and Zhejiang in this region have cultivated a number of machine tool enterprises with international competitiveness. Relying on the strong manufacturing foundation of the Pearl River Delta, South China has formed unique advantages in the fields of special-purpose machine tools and numerical control systems. Central China, with Wuhan as the core, has traditional advantages in heavy-duty machine tools and special processing equipment. The Northeast China region, by virtue of its solid industrial foundation, maintains a leading position in the fields of precision machine tools and functional components. This pattern of regional differentiated competition is conducive to optimizing resource allocation and avoiding homogeneous competition.

Changes in downstream application fields have also profoundly affected the development trajectory of the machine tool industry. In 2024, the automotive industry remained the largest application market for machine tools, accounting for 25.6%. Among them, the rapid development of new energy vehicles has driven the processing demand for high-precision parts such as battery casings and motor shafts. The electronics industry accounted for 21.8%, mainly serving the processing of 3C electronic product components, which has extremely high requirements for the intelligence and flexibility of machine tools. It is worth noting that although the aerospace field currently accounts for only 4.3%, its growth rate has reached 10%. With the advancement of domestic large aircraft projects, the demand for high-end numerically controlled machine tools such as five-axis machining centers will be continuously released. The medical equipment industry maintained a stable growth of 4%, and its strict requirements on processing accuracy and surface quality are promoting the continuous upgrading of machine tool technology.

In recent years, national macro-policies have continuously focused on the replacement of old machine tool equipment with new ones and technological upgrading, promoting the industry to develop in the direction of digitalization, intelligence, and low-carbonization. 2024 became a crucial year with intensive policy introductions; from the beginning to the end of the year, a series of important documents were successively released, providing clear guidance for the transformation and upgrading of the machine tool industry. In April, the Ministry of Industry and Information Technology issued the "Implementation Plan for Promoting Equipment Renewal in the Industrial Sector", which clearly proposed to "improve product quality with reliability as the core", focus on key industries such as machinery, electronics, and automobiles, and promote the implementation of policies in fields such as industrial machine tools (the "mother machines" of industry). This policy directly addresses the structural contradiction in the machine tool industry, namely the oversupply of low-end products and the shortage of high-end products, and forces enterprises to upgrade their technologies by raising quality standards.

The equipment renewal policy reached a climax in March 2024, when the State Council issued the "Action Plan for Promoting Large-Scale Equipment Renewal and Trade-in of Consumer Goods". It set a quantitative target that the investment scale in equipment in industries such as industry by 2027 would increase by more than 25% compared with 2023, and at the same time required that the numerical control rate of key processes in large-scale industrial enterprises should exceed 75%. This policy is of milestone significance, as it systematically arranged equipment renewal at the national level and created a huge stock replacement market for the machine tool industry. According to estimates, about 60% of China's existing machine tool equipment has been in use for more than 10 years. In accordance with policy requirements, these equipment will be gradually replaced by new high-efficiency, intelligent, and green machine tools, releasing a market space of hundreds of billions of yuan.

The path of technological upgrading has been clearly outlined in policy documents. The Implementation Plan for Promoting Equipment Renewal in the Industrial Sector, jointly issued by seven ministries and commissions including the Ministry of Industry and Information Technology (MIIT), explicitly states: "Focusing on the transformation of links such as production operations, warehousing and logistics, and quality control, we will promote the renewal of general intelligent manufacturing equipment such as numerical control (NC) machine tools, basic manufacturing equipment, additive manufacturing equipment, and industrial robots." This policy places machine tools at the core of the intelligent manufacturing ecosystem, emphasizing their coordinated development with other intelligent equipment. In terms of specific technological directions, high-end products such as five-axis machining centers, turn-mill composite machining centers, and heavy-duty NC machine tools have been repeatedly mentioned, reflecting the country's firm determination to break through "bottleneck" technologies.

The concept of green manufacturing has been deeply integrated into industrial policies. In February, the State Council released the Opinions on Accelerating the Construction of a Waste Recycling System, which proposes to "promote the development of the remanufacturing industry in traditional fields such as auto parts, construction machinery, and machine tools, and explore high-end equipment remanufacturing in new fields such as aero-engines and industrial robots." This policy guides the machine tool industry to transform into a circular economy model, extending product life cycles through remanufacturing, reducing resource consumption and environmental pollution. At the end of 2023, the National Development and Reform Commission (NDRC) issued the Guidance Catalog for Industrial Structure Adjustment (2024 Version), which for the first time upgraded NC machine tools from the machinery category to a separate entry in the encouraged category. At the same time, it revised the content of machine tool products in the restricted and eliminated categories, promoting the industry's advancement toward high-end development through industrial structure adjustment.

Driven by policy dividends, machine tool enterprises have actively adjusted their strategic layouts. In 2024, the industry showed three main development threads:

M&A and integration to address weaknesses: Examples include Yuhuan NC's acquisition of shares in Hunan South Machine Tool and United Grinding's acquisition of GF Machining Solutions. These moves enhance comprehensive competitiveness through resource integration.

Focused breakthroughs in "bottleneck" technology areas: Many enterprises have increased R&D investment in key technologies such as five-axis linkage and high-precision gratings.

Accelerated expansion into overseas markets: For instance, Brother Machine Tools built a factory in India, and Nidec Machine Tools put into production in Pinghu, Zhejiang. These global layouts help hedge against the risk of fluctuations in the domestic market.

These strategic initiatives are highly aligned with policy orientations, forming a positive interaction pattern led by the government and driven by the market.

The integration of emerging technologies with machine tools has become an important direction encouraged by policies. The "Industrial Machine Tool +" production-demand matching campaign for thousands of enterprises across hundreds of industries, launched by the MIIT, aims to promote the demonstration application of innovative products in fields such as aerospace and new energy. New infrastructure such as 5G and industrial internet provides technical support for machine tool networking and data collaboration, facilitating the development of new models such as flexible production lines and shared factories. Driven by both policies and technologies, the machine tool industry is shifting from single-machine sales to providing overall solutions, and service-oriented manufacturing is beginning to take shape. This transformation not only expands the industry's boundaries but also improves enterprises' profitability and risk resistance capabilities.

The competitive landscape of China's machine tool market is undergoing a profound restructuring, showing a diversified pattern characterized by foreign capital dominating the high-end segment, domestic products accelerating substitution, and fierce competition in the low-end segment. The 2024 market landscape can be clearly divided into three tiers:

The first tier consists of international giants such as Doosan, DMG MORI, Mazak, and Grob, occupying approximately 12% of the high-end market share.

The second tier includes leading domestic enterprises such as Beijing Jingdiao, Chuangshiji, Qinchuan Machine Tool, and Haitian Precision Machinery, holding 28% of the mid-end market share.

The third tier comprises a large number of small and medium-sized private enterprises, which compete fiercely in the low-end market. Their market share dropped from 65% in 2019 to 60% in 2024, indicating a gradual increase in industry concentration.

This "pyramid-shaped" competitive structure reflects the development stage and transformation/upgrading path of China's machine tool industry.

Competition in the high-end market is the most eye-catching. With a century of technological accumulation, international machine tool giants hold an absolute advantage in high-value-added fields such as aerospace and precision molds. Taking five-axis machining centers as an example, their core technologies have long been monopolized by European and American enterprises such as DMG MORI and Grob, with prices often exceeding 10 million yuan. These enterprises not only provide high-precision and high-reliability equipment but also possess the capability of integrating complex functions, enabling them to offer complete solutions to customers. However, as Western countries tighten export controls on high-end machine tools, the market share of international giants in China has shown a downward trend, creating strategic opportunities for domestic substitution. In 2024, high-end NC machine tools from enterprises such as Kede NC and Shenyang Machine Tool began to enter key fields such as aerospace and military industry, marking substantial progress in domestic breakthroughs.

The mid-end market has become the main battlefield for domestic machine tool brands. Taking Haitian Precision Machinery as an example, the company achieved steady revenue growth in 2024. By focusing on a differentiated competition strategy, it has established a solid market position in fields such as auto parts and general machinery. Beijing Jingdiao has continued to deepen its presence in the precision machining field, and its five-axis high-speed machining center JDMR80 has been widely used in the 3C industry. These leading domestic enterprises generally adopt an "import substitution" strategy, gradually eroding the market space of foreign brands through cost-performance advantages. Notably, competition in the mid-end market has shifted from pure price wars to all-round competition in technology, services, and brands. Enterprises have increased R&D investment to improve product reliability and stability, narrowing the gap with international advanced levels.

The low-end market is experiencing an accelerated reshuffle. A large number of small private enterprises compete fiercely in the traditional mechanical processing field, with serious product homogeneity and continuous compression of profit margins. Under the pressure of economic downturn in 2024, demand in the low-end market shrank significantly, and some enterprises with low technological content and weak financial strength were forced to exit the market. Meanwhile, some forward-looking enterprises have begun to penetrate the mid-end market through differentiated strategies—such as focusing on industry-specific machine tools or providing customized services—gradually breaking away from the quagmire of low-end vicious competition. This "survival of the fittest" market mechanism is conducive to optimizing the industry structure and improving resource allocation efficiency, but it also brings social issues such as increased employment pressure in the short term.

As an important part of the machine tool industry, the cutting tool market also presents an obvious hierarchical competitive pattern:

European and American brands such as Sandvik and Kennametal dominate the high-end customized cutting tool market, maintaining high profit margins through technological leadership.

Japanese and South Korean enterprises such as Mitsubishi Materials and TaeguTec occupy the mid-end market with cost-performance advantages.

Domestic enterprises such as Zhuzhou Diamond mainly compete in the low-end market.

In 2024, the overall scale of the cutting tool industry declined by 2%, with serious overcapacity and homogeneous competition, and low-end small factories gradually withdrew from the market. However, super-hard cutting tools maintained an upward trend in production and sales due to their advantages in high-speed and precision machining, reflecting the market's sustained demand for high-performance cutting tools.

Regional competition has shown new characteristics:

East China, centered on Shanghai and Jiangsu, has formed industrial clusters for NC systems and precision machine tools.

South China, relying on Guangdong's strong manufacturing foundation, has advantages in the field of special-purpose machine tools.

Central China is distinctive in heavy-duty machine tools.

Northeast China maintains its traditional advantages in the field of functional components.

This regional differentiated competition avoids homogeneous internal friction and is conducive to forming an industrial ecosystem of coordinated development. At the same time, local governments have also introduced supporting policies—such as establishing industrial funds and building innovation centers—to support the growth of local machine tool enterprises. Competition and cooperation among regions jointly promote the overall progress of the industry.

Looking ahead, China’s machine tool industry will develop in the directions of high-endization, intelligence, greenization, and globalization, with continuous optimization of industrial structure and significant enhancement of innovation capabilities. The growth in demand for high-end products and the phasing out of low-end production capacity will advance in parallel; driven by both policy incentives and technological breakthroughs, market concentration is expected to further increase. The national "Two Priorities" strategy (national major strategies & projects, and capacity building for security in key fields) and the "Two New Directions" (new-quality productive forces and new technology fields) will create new growth drivers for the machine tool industry—particularly in strategic sectors such as aerospace, new energy, and semiconductors. Demand for high-precision, multi-functional machine tools in these fields will see explosive growth.

Technological breakthroughs will be the key to future competition. High-end products such as five-axis machining centers, ultra-precision machine tools, and multi-tasking machine tools are the main focus of domestic substitution efforts. As R&D investment continues to increase, it is expected that by 2025, the application of domestic high-end machine tools in "bottleneck" fields such as military industry and nuclear power will expand further. The pace of intelligent transformation will accelerate: the deep integration of technologies such as industrial internet and artificial intelligence (AI) with machine tools will give rise to a new generation of intelligent numerical control (NC) systems, enabling value-added services such as remote operation and maintenance, and predictive maintenance. The application of digital twin technology will upgrade machine tools from simple processing equipment to intelligent manufacturing units, significantly improving production efficiency and resource utilization. These technological innovations will not only transform product forms but also reshape the industry’s value chain and business models.

The expansion of application scenarios will open up new market space. The rise of emerging industries such as new energy vehicles, humanoid robots, and commercial aerospace has placed higher demands on machine tools. Taking humanoid robots as an example, the processing of their core components—such as precision reducers and high-performance servo motors—requires ultra-high-precision machine tools, and demand in this market has only just begun to release. The rapid development of the commercial aerospace sector will also drive growth in demand for specialized machine tools, such as those used for processing large structural parts and cutting lightweight materials. Machine tool enterprises need to closely monitor changes in downstream industries, lay out plans for emerging fields in advance, and develop specialized equipment and process solutions. This application-oriented innovation model helps avoid homogeneous competition and establish differentiated advantages.

Global layout will become a standard practice for leading enterprises. In 2024, top manufacturers significantly accelerated their overseas expansion—for instance, the completion and opening of technology centers in Malaysia. These cases reflect that capable enterprises are actively building global marketing networks. The accelerated industrialization process in countries along the "Belt and Road" has created strong demand for cost-effective Chinese machine tools, providing new impetus for export growth. At the same time, acquiring core technologies through the acquisition of outstanding international enterprises is also an important path to achieving leapfrog development. In the future, Chinese machine tool enterprises will gradually upgrade from product export to technology export and standard export, and their position in the global value chain will continue to rise. However, this process also faces challenges such as trade barriers and cultural integration, requiring enterprises to develop stronger international operation capabilities.

The concept of sustainable development will be deeply integrated into the entire product life cycle. The promotion and application of circular economy models such as green manufacturing and remanufacturing will help the machine tool industry continuously reduce carbon emission intensity. Innovative achievements such as new environmentally friendly cutting fluids and dry cutting technology will reduce environmental pollution during production. Higher energy efficiency standards will drive enterprises to develop more energy-saving products—for example, spindle units using direct-drive technology can save more than 20% energy compared with traditional structures. Carbon footprint management has become a new competitive dimension; leading enterprises have begun to green their supply chains to cope with increasingly strict environmental regulations and international carbon tariff barriers. This green transformation is both a challenge and an opportunity, and will reshape the industry’s competitive landscape.

The industrial ecosystem will become more open and collaborative. Collaborative innovation between complete machine enterprises, functional component suppliers, and NC system developers will become increasingly close, as they jointly overcome key technological bottlenecks. The industry-university-research cooperation model will continue to innovate—for example, enterprise-led innovation consortia play an important role in solving common technological problems in the industry. Progress in supporting industries such as industrial software and sensors provides a solid foundation for the intelligentization of machine tools. Platform-based enterprises in the industry have begun to emerge, integrating industrial chain resources to provide one-stop services for customers. This trend of ecosystem-based development helps optimize the allocation of innovation resources, accelerate technological iteration and achievement transformation, and enhance the overall competitiveness of China’s machine tool industry.

The above is a comprehensive analysis of the development of China’s machine tool industry in 2025. From the improvement of NC rate to the optimization of industrial structure, and from policy-driven to market-led growth, China’s machine tool industry is undergoing a profound transformation. Against the backdrop of global competition and the technological revolution, Chinese machine tool enterprises can only gain the initiative in fierce market competition and achieve the leap from a "large manufacturing country" to a "powerful manufacturing country" by adhering to innovation-driven development, prioritizing quality, and pursuing green growth. In the next few years, as policy dividends continue to be released, technological bottlenecks are gradually overcome, and application scenarios are expanded, China’s machine tool industry is expected to enter a new stage of high-quality development, providing solid support for the construction of a powerful manufacturing country.

Source: Future Think Tank

Free Service Hotline:

Free Service Hotline: Email:allisonho@foxmail.com

Email:allisonho@foxmail.com Address:1st Floor, Building E, No. 6, Hongye South 2nd Road, Tangxia Town, Dongguan City, Guangdong Province

Address:1st Floor, Building E, No. 6, Hongye South 2nd Road, Tangxia Town, Dongguan City, Guangdong Province Fax:0769-82865290

Fax:0769-82865290